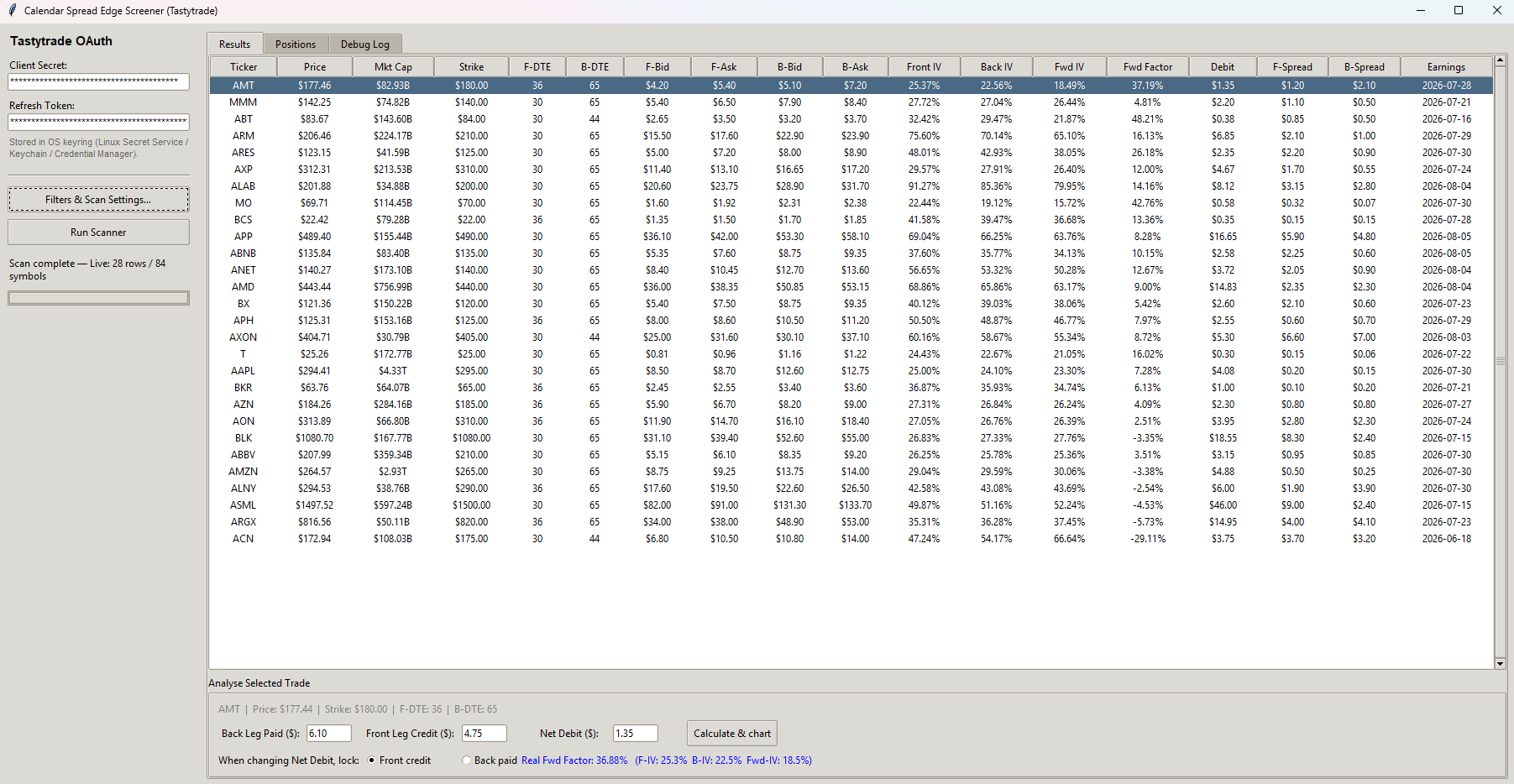

Live Option Chain Scanning

Rank thousands of Tastytrade calendar spread setups by Forward Factor in real-time.

Click to enlarge

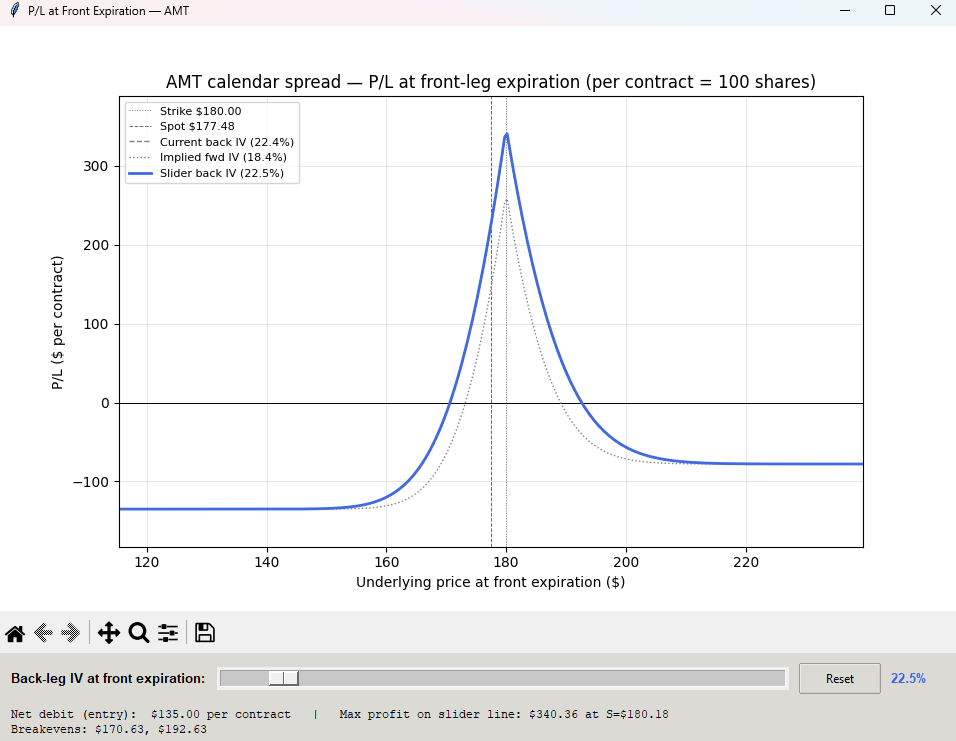

Interactive Forward Factor Calculator & P/L

Visualize your potential profit and loss exactly at the front-leg expiration. The interactive Matplotlib integration includes a dynamic slider to adjust the back-leg implied volatility, instantly recalculating breakevens, max profit, and curve structure.

Click to enlarge

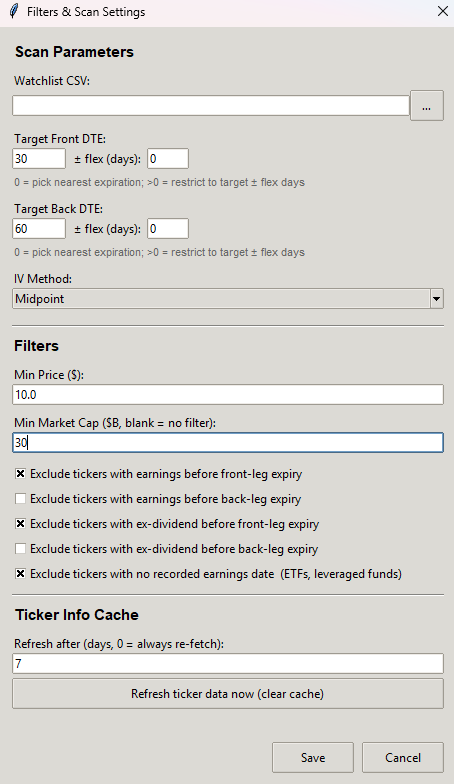

Click to enlarge

Advanced Targeting & Filters

Define strict parameters for your scans. Target specific days-to-expiration (DTE) with flexible window tolerances, filter by minimum underlying price or market cap, and utilize the yfinance integration to automatically exclude tickers with upcoming earnings or ex-dividend dates to avoid event-driven volatility crush.